Ozempic users are going crazy for deli meat, fries, and handbags

GLP-1s are life-changing drugs, transforming not only waistlines but also identity and indulgence.

Hello hello! It’s Dan Frommer, back with The New Consumer, back home in LA after a maybe-too-perfect fall week in New York.

It was great to see many of you around the city last week, including the excellent New Fare Partners dinner at Una Pizza Napoletana, the Human Ventures / Casa Komos roast for Alex Heath, and Ben Settle’s stylish hang at Undercote. I think I was the first paying Sourmilk yogurt customer at their Happier Grocer retail debut — neat. And as always, major gratitude to my Consumer Trends collaborators at Coefficient Capital for letting me take over their big office table between meetings. We’ll be launching our next big report in a few weeks.

Ozempic and other GLP-1 weight-loss drugs have not torpedoed the food and CPG industries the way some had feared. But they do drive meaningful shifts in users’ spending.

I recently watched a new, hourlong presentation from Circana about GLP-1 users’ changing grocery and retail shopping habits, based on its checkout-scanner and omnichannel shopping data (link to full slide deck).

Here are some of the highlights.

The number of Americans taking GLP-1 drugs continues to grow substantially. There’s no official tally, but Circana believes that 23% of US households — about 30 million — had at least one GLP-1 user in September, suggesting there are tens of millions of users. By 2030, five years from now, it expects GLP-1 households to purchase 35% of food sold in the US (measured by units), up from 24% today.

GLP-1 usage continues to shift toward weight loss and cosmetic/aesthetic/casual/microdosing usage, away from diabetes management. As usage has grown, 78% of GLP-1 users now cite weight loss as a motivating factor for using the drugs, up from 37% in 2021. Meanwhile, 43% cite diabetes as a motivating factor today, down from 75% in 2021. Almost half of users are now “weight only,” twice the proportion as two years ago.

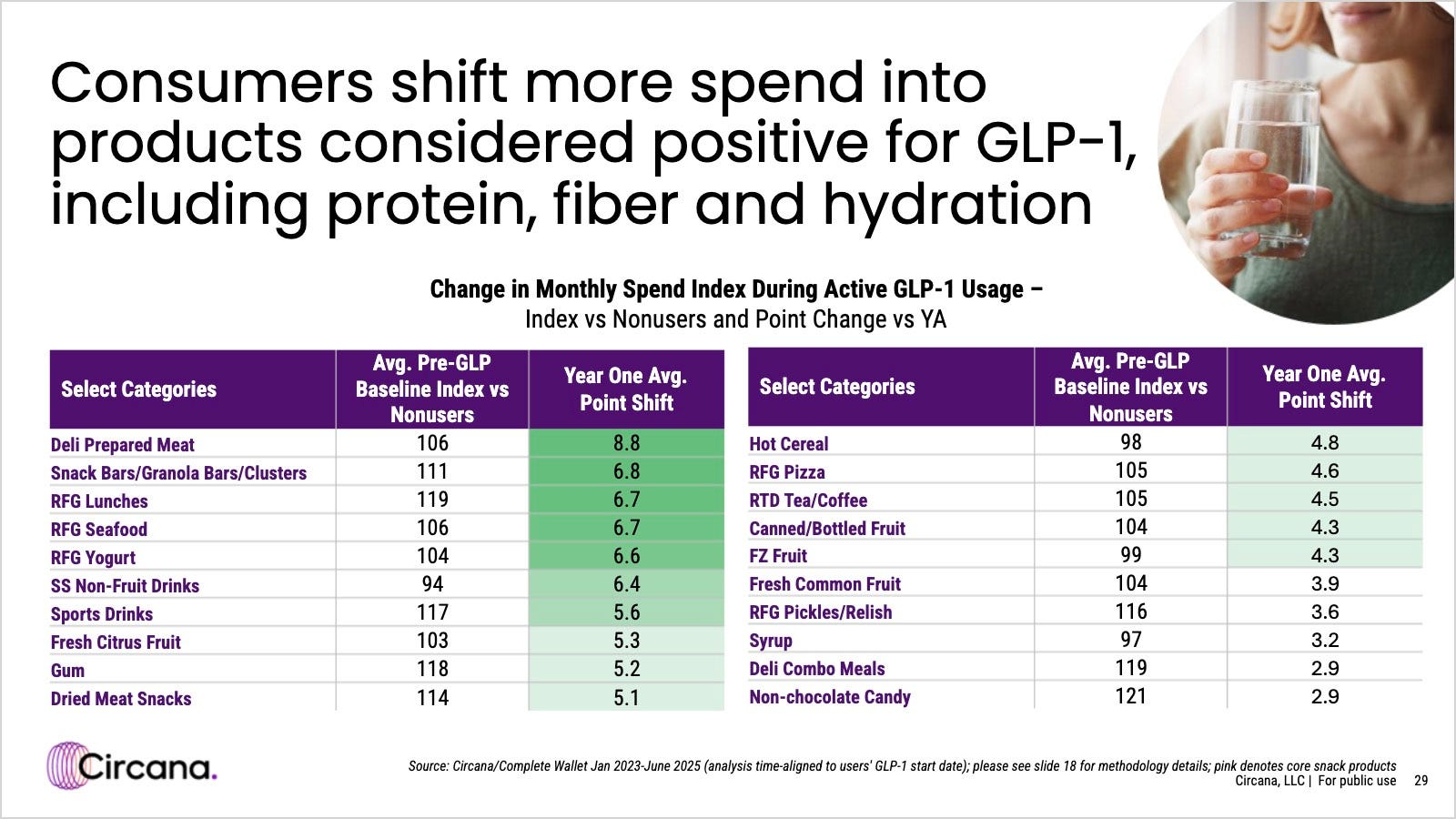

Deli meats are a big winner as GLP-1 users shift their grocery spending toward products high in protein and fiber. Protein is a top food trend for many consumers, but especially for GLP-1 users, who need to preserve muscle mass while losing weight.

The top-gaining categories among active GLP-1 users, as tracked by Circana, include prepared deli meats; snack bars and granola; refrigerated lunches, seafood, and yogurt; beverages, including sports drinks; fresh citrus; gum; and dried meat snacks.

Here’s how to read the data on these slides, btw: The “average pre-GLP baseline index” shows how GLP-1 users’ spending compares to the average US household (100) before they started using the medication. So in the case of deli prepared meats, active GLP-1 users were at 106 to begin — roughly 6% bigger shoppers than the average household. Adding another 8.8 points in a year, then, as they did in the case of deli meat, is pretty significant.

Fries — the great equalizer. Balancing sensible foods with treats, weight-loss focused GLP-1 users over-index in eating protein-rich eggs for breakfast (20% of the time) and chicken for lunch.

But they way over-index in eating fries at lunch (12% of the time) and cookies at dinner. Hey, why not — those calories were earned!